23 Sep 2010, 9am sharp. Took out my branch trimmer started snipping away the deadwoods. Plucks some low hanging fruits for a snack. And the bull hit the sack.

The next few days, planted a few new seeds, give 'em a good watering. Starting to germinate. Waiting for a good harvest come the harvesting season.

It is an art. There is no exact science about it. It is about tilting the odds in your favour. Once you lost your mojo, once you can no longer read the lines clearly, once you don't like how the story is unfolding, then the odds are no longer in your favour. Best to reduce positions and re-assess the situation. Feel the mojo.

I think the bull has woke up from his little nap, but still feeling a bit groggy. Perhaps will laze around munching grass before trotting on. Up or down, that is the question.

Tuesday 28 September 2010

Wednesday 22 September 2010

Taking some dough off the table

The market is starting to look weary. I think it is time to reduce open positions and consolidate fund while looking for new opportunities.

KPJ made new low. Testing ema81. Is it time to panic? Yeah, potential to meet 3.24~3.26 support. Was I waiting for ages there! Should I cut and wait at 3.24~3.26? Nah, going to scoop up some more :)

Sometime rotating trades among few favourite counters is sufficient to earn peanuts off the market. It is a big ocean out there with thousands of species of fishes. Get to know a few fishes well and you can reel them in with better ease. Of course sometime I feel more adventurous and go for electric eel or puffer fish.

Back to KPJ. Initial foray was at 2.6x level. I think by now my effective entry is a good figure below 2.00 after a few churns, not inclusive the dividends received. Looking to top up should KPJ tests major support. Fundamentals are intact.

In the meantime, time to rebalance my portfolio. Shakes off a few deadwoods. Reduce some positions. Top up my fav REIT counter and keep fingers crossed for budget 2011 goodies. The goodies gotta come sooner or later if the fed is serious about making our market more competitive.

KPJ made new low. Testing ema81. Is it time to panic? Yeah, potential to meet 3.24~3.26 support. Was I waiting for ages there! Should I cut and wait at 3.24~3.26? Nah, going to scoop up some more :)

Sometime rotating trades among few favourite counters is sufficient to earn peanuts off the market. It is a big ocean out there with thousands of species of fishes. Get to know a few fishes well and you can reel them in with better ease. Of course sometime I feel more adventurous and go for electric eel or puffer fish.

Back to KPJ. Initial foray was at 2.6x level. I think by now my effective entry is a good figure below 2.00 after a few churns, not inclusive the dividends received. Looking to top up should KPJ tests major support. Fundamentals are intact.

In the meantime, time to rebalance my portfolio. Shakes off a few deadwoods. Reduce some positions. Top up my fav REIT counter and keep fingers crossed for budget 2011 goodies. The goodies gotta come sooner or later if the fed is serious about making our market more competitive.

Friday 17 September 2010

5106 AXREIT

AXIS REIT, 5106 AXREIT

Yep. A really long shot. Price did not retrace with new issue listing. Be a good chum and retrace a bit. Even RM2.00 will be swell.

Waiting for a blue moon seems a lot easier and certain. Today is Sept 17. Budget 2011 will be announced on Oct 15. Only 3 weeks entry window left, betting on the WHT to be reduced or abolished. That will be a catalyst for upward price target re-rating.

If the proposal for more speedy and more frequent fund size increase is allowed, given AXREIT track record of yield accretive acquisitions, I would think RM 2 Billion mark would be achieved sooner rather than latter. DPS would easily surpass 20 sen mark.

Down risk? Nothing serious :)

Yep. A really long shot. Price did not retrace with new issue listing. Be a good chum and retrace a bit. Even RM2.00 will be swell.

Waiting for a blue moon seems a lot easier and certain. Today is Sept 17. Budget 2011 will be announced on Oct 15. Only 3 weeks entry window left, betting on the WHT to be reduced or abolished. That will be a catalyst for upward price target re-rating.

If the proposal for more speedy and more frequent fund size increase is allowed, given AXREIT track record of yield accretive acquisitions, I would think RM 2 Billion mark would be achieved sooner rather than latter. DPS would easily surpass 20 sen mark.

Down risk? Nothing serious :)

Tuesday 14 September 2010

Charging Bull

Don't know how to describe the KLCI bull. Unbelievable. What can I say? Enjoy the ride (if you are in the right counters).

NCB and SCABLE have moved. Practically everything moved. Just a question of magnitude and momentum.

Yeah, just going to enjoy the ride. Not going to enter any new trades for the time being. Not with the bull charging. Sigh, mixed fortune. How nice if I have picked all the right counters and watch the syndicates rotate amongst those counters. Everyday at least one counter +5% or more while the rest consolidates.

But I am going to try my luck with 5106. This is going to be a really really long shot.

Details of corporate proposal:

68,819,800 new units in Axis Real Estate Investment Trust ("Axis-REIT") ("Final Tranche Placement Units"), representing about 22.4% of the existing units in Axis-REIT ("Units") in circulation of 307,081,200 Units at an issue price of RM1.97 per Unit, being the final tranche of the placement units of 120,000,000 Units

Listing Date: 15/09/2010

NCB and SCABLE have moved. Practically everything moved. Just a question of magnitude and momentum.

Yeah, just going to enjoy the ride. Not going to enter any new trades for the time being. Not with the bull charging. Sigh, mixed fortune. How nice if I have picked all the right counters and watch the syndicates rotate amongst those counters. Everyday at least one counter +5% or more while the rest consolidates.

But I am going to try my luck with 5106. This is going to be a really really long shot.

Details of corporate proposal:

68,819,800 new units in Axis Real Estate Investment Trust ("Axis-REIT") ("Final Tranche Placement Units"), representing about 22.4% of the existing units in Axis-REIT ("Units") in circulation of 307,081,200 Units at an issue price of RM1.97 per Unit, being the final tranche of the placement units of 120,000,000 Units

Listing Date: 15/09/2010

Unbelievable

Don't know how to describe the KLCI bull. Unbelievable. What can I say? Enjoy the ride (if you are in the right counters).

NCB and SCABLE have moved. Practically everything moved. Just a question of magnitude and momentum.

Yeah, just going to enjoy the ride. Not going enter any new trades for the time being. Not with the bull charging. Sigh, mixed fortune. How nice if I have picked all the right counters and watch the syndicates rotate amongst the counters. Everyday at least a counter +5% or more while the rest consolidates.

But I am going to try my luck with 5106. This is going to be a really really long shot.

NCB and SCABLE have moved. Practically everything moved. Just a question of magnitude and momentum.

Yeah, just going to enjoy the ride. Not going enter any new trades for the time being. Not with the bull charging. Sigh, mixed fortune. How nice if I have picked all the right counters and watch the syndicates rotate amongst the counters. Everyday at least a counter +5% or more while the rest consolidates.

But I am going to try my luck with 5106. This is going to be a really really long shot.

Saturday 11 September 2010

Q2'10 updates

Now that reporting season for Q2 2010 is over...

KPJ seems to has a new dividend policy; quarterly dividend. 6.5 sen over past 2 quarters or 13.0 sen annualized. Annualized EPS is 21.46 sen giving a PER of 16.3x at RM3.50 closing price. Patiently waiting for the latest round of asset injection into Al'Aqar REIT for share swap to be completed.

ARREIT. 1H10 yields 3.86 sen or 7.72 p.a. giving a neat 8.58% GDY at RM0.90. That is pretty much it, being the nature of REIT... mundane, unexciting. But the more fun-lovin' REITs have slightly more life. We'll see in due time if the PKNS assets injection provide the needed boost. Looks good I last checked :)

KPJ seems to has a new dividend policy; quarterly dividend. 6.5 sen over past 2 quarters or 13.0 sen annualized. Annualized EPS is 21.46 sen giving a PER of 16.3x at RM3.50 closing price. Patiently waiting for the latest round of asset injection into Al'Aqar REIT for share swap to be completed.

ARREIT. 1H10 yields 3.86 sen or 7.72 p.a. giving a neat 8.58% GDY at RM0.90. That is pretty much it, being the nature of REIT... mundane, unexciting. But the more fun-lovin' REITs have slightly more life. We'll see in due time if the PKNS assets injection provide the needed boost. Looks good I last checked :)

Thursday 9 September 2010

Trading idea

SIME 4197

Placed on my watchlist since week2 Aug. Good pattern formation with indicators hooking up.

At a cross road. Trapped between a downtrend line and ema-81w, FB23.6%. Last few candles and indicators are looking nice.

PARKSON 5657

Placed on my watchlist since mid-Aug. Been under accumulation with increasing urgency towards end-Aug.

Looking gold.

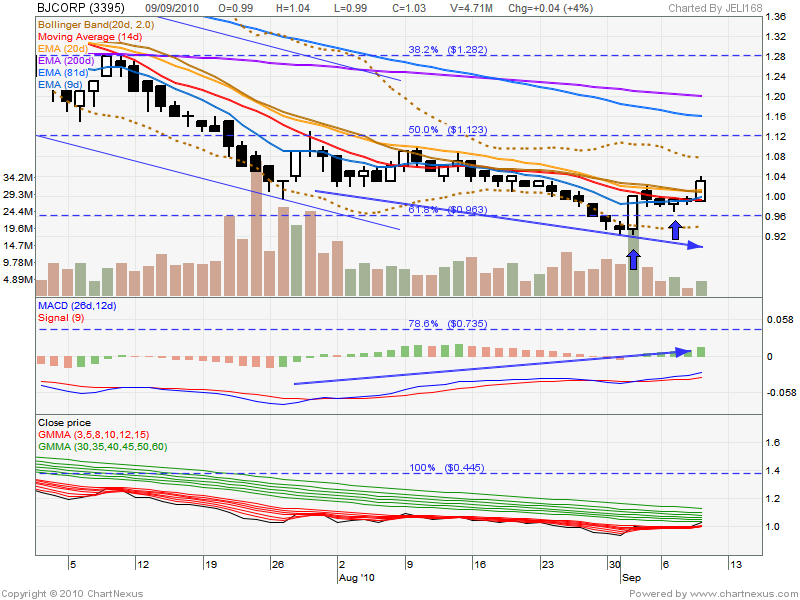

BJCORP 3395

Placed on my watchlist since Sept 8. Closed above ceiling today.

That's kind of a hurry :(

NCB 5509

Placed on watchlist on Sept 8. Closed above ceiling today.

That's kind of a hurry :(

SCABLE 5170

Placed on watchlist on Sept 8. Formation setting up. Did not close above ceiling today. Good! No hurry ok? Let me watch first for a day or three...

Placed on my watchlist since week2 Aug. Good pattern formation with indicators hooking up.

At a cross road. Trapped between a downtrend line and ema-81w, FB23.6%. Last few candles and indicators are looking nice.

PARKSON 5657

Placed on my watchlist since mid-Aug. Been under accumulation with increasing urgency towards end-Aug.

Looking gold.

BJCORP 3395

Placed on my watchlist since Sept 8. Closed above ceiling today.

That's kind of a hurry :(

NCB 5509

Placed on watchlist on Sept 8. Closed above ceiling today.

That's kind of a hurry :(

SCABLE 5170

Placed on watchlist on Sept 8. Formation setting up. Did not close above ceiling today. Good! No hurry ok? Let me watch first for a day or three...

Tuesday 7 September 2010

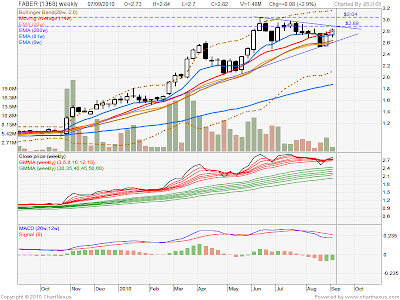

1368 FABER

Faber Group Berhad, 1368 FABER

p/s: For "Y".

Trading play. Healthcare sector - integrated facility management, IFM. Laundromat for Malaysia government's hospitals and some hospitals in Saudi A. MY GH laundromat contract expiring, renewal expected soon. Around October/November 2010. Faber could be a SELL-on-news play, so extra caution is advised trading this counter.

Weekly chart. The chart is less congested. Long uptrend line support test. Indicators are hooking up. IR 2.89, R1 3.04.

Trading note. Personally no trading position in Faber. Prefers KPJ for health sector exposure.

p/s: For "Y".

Trading play. Healthcare sector - integrated facility management, IFM. Laundromat for Malaysia government's hospitals and some hospitals in Saudi A. MY GH laundromat contract expiring, renewal expected soon. Around October/November 2010. Faber could be a SELL-on-news play, so extra caution is advised trading this counter.

Daily chart. C 2.98 & F 2.50. The last 7 candles are bullish with strong price/volume momentum. Closed above immediate downtrend line. Immediate resistance, IR 2.89, R1 2.98, R2 3.04.

Weekly chart. The chart is less congested. Long uptrend line support test. Indicators are hooking up. IR 2.89, R1 3.04.

Trading note. Personally no trading position in Faber. Prefers KPJ for health sector exposure.

Monday 6 September 2010

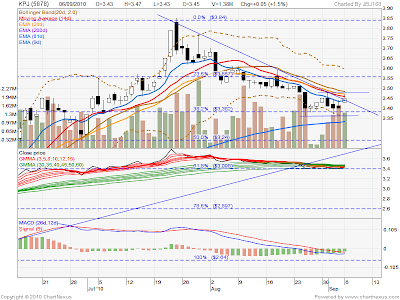

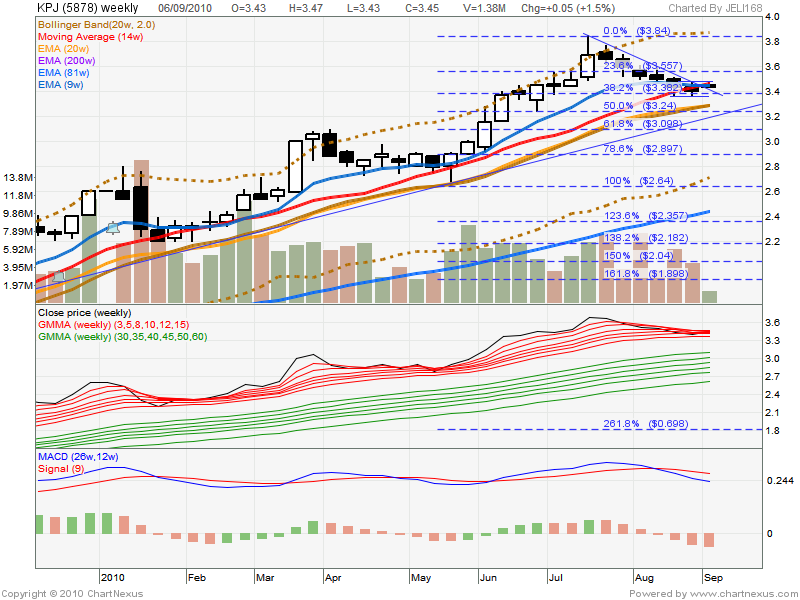

5878 KPJ

KPJ Healthcare, 5878 KPJ

When it comes to KPJ Healthcare, it is hard for me not to violates one of the most fundamental rule in stock investment. Do NOT make love with your stocks. No, not that kind of love making. But love as in attaching a sentimental value to the stock. Trade by charts. Invest by facts.

Since rising from the ashes in 2006, KPJ has not look back. Revenue increased from RM 222M in Q406 to RM 376M in Q110. EPS leaped from 5.65 sen in Q406 to 13.59 sen in Q409 (before 2:1 share split & 1:4 bonus issue), or 5.09 sen adjusted. Q110 EPS was 5.19. Dividends dished during the same period was nothing short of fantastic by my standard. 51 sen in cash, 30:100 alaqar shares, 1:4 free warrant. The alaqar shares is a dividend that keeps on giving.

Alas, my affair with KPJ Healthcare only started in Q110 after keeping it in radar for a good duration in 2009, after I am assured of the company's growth strategy, execution and dividend policy. My view is that healthcare industry in Malaysia is just exiting from it's infancy and KPJ Healthcare is positioned to ride this wave. KPJ's venture to Indonesia is also a plus point with proven execution.

Daily chart. KPJ retraced to FB23.6% after hitting a high of 3.85, hovered for a while before drifting down to FB38.2%. Floor 3.36 & Ceiling 3.48 found. The last candle closed above downtrend line. Indicators showing signs of hooking up. Looks good for a low risk re-entry.

Weekly chart. The long uptrend line suggests a potential retrace to 3.28. KPJ has been under sustained selling pressure for 6 weeks straight making a lower low. However, it failed to make a lower low on the 6th week. Is the bull winning? Week 7 opened with a white candle bucking the immediate downtrend line.

Trading note. Exited position when FB23.6% failed. Low risk re-entry on 3-Sep after establishing C&F and FB38.2% support.

When it comes to KPJ Healthcare, it is hard for me not to violates one of the most fundamental rule in stock investment. Do NOT make love with your stocks. No, not that kind of love making. But love as in attaching a sentimental value to the stock. Trade by charts. Invest by facts.

Since rising from the ashes in 2006, KPJ has not look back. Revenue increased from RM 222M in Q406 to RM 376M in Q110. EPS leaped from 5.65 sen in Q406 to 13.59 sen in Q409 (before 2:1 share split & 1:4 bonus issue), or 5.09 sen adjusted. Q110 EPS was 5.19. Dividends dished during the same period was nothing short of fantastic by my standard. 51 sen in cash, 30:100 alaqar shares, 1:4 free warrant. The alaqar shares is a dividend that keeps on giving.

Alas, my affair with KPJ Healthcare only started in Q110 after keeping it in radar for a good duration in 2009, after I am assured of the company's growth strategy, execution and dividend policy. My view is that healthcare industry in Malaysia is just exiting from it's infancy and KPJ Healthcare is positioned to ride this wave. KPJ's venture to Indonesia is also a plus point with proven execution.

Daily chart. KPJ retraced to FB23.6% after hitting a high of 3.85, hovered for a while before drifting down to FB38.2%. Floor 3.36 & Ceiling 3.48 found. The last candle closed above downtrend line. Indicators showing signs of hooking up. Looks good for a low risk re-entry.

Weekly chart. The long uptrend line suggests a potential retrace to 3.28. KPJ has been under sustained selling pressure for 6 weeks straight making a lower low. However, it failed to make a lower low on the 6th week. Is the bull winning? Week 7 opened with a white candle bucking the immediate downtrend line.

Trading note. Exited position when FB23.6% failed. Low risk re-entry on 3-Sep after establishing C&F and FB38.2% support.

Sunday 5 September 2010

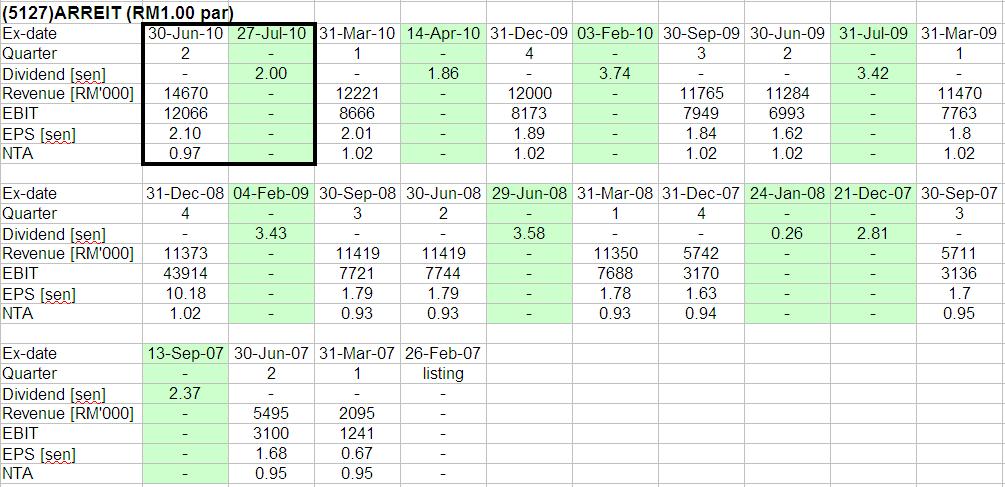

5127 ARREIT

Amanah Raya REIT, 5127 ARREIT

Weekly chart. There was a 4 weeks selldown in Apr/May. Followed by 3 mths sideway accumulation with increasing vol and higher high candles. Floor&Ceiling has also formed. This is what attracted my attention in the first place :)

This week closed with bullish macd divergence above ceiling. Expecting it to visit recent high of RM 0.925.

Salient details:

Listed on 26 February 2007, par value RM 1.00

Currently own 15 properties.

Current DPS around 7.6 sen, or 8.5% gross yield at RM 0.880 entry.

Catalyst:

PKNS injecting 3 properties valued at RM 270M into ARREIT with expected Q410 completion. Partial new share, partial cash payment. Not sure if the 3 new properties are yield accretive, but back of the envelope calculation (which is likely flawed) revealed so much...

New share issue: 122,727,273 @RM 0.880

Existing share issue: 573,219,858

Loan drawdown: RM 162M

*Assumption - new properties yield 8.5%

current market cap: 573,219,858*0.88= RM 504.43M;

market cap increase: (270-162)/504.43= +20.41%;

issue increase: 122,727,273/573,219,858= +21%;

new cap: 695,947,131*0.88= RM 612.43M;

DY accretive: 162/612.43 = +26.45% (assuming 8.5% DY);

--> theoritical target price: 0.88*1.2645= RM 1.11 @8.5% or RM 1.34 @7.0% DY

--> theoritical cap appreciation: 1.11/0.88= +26.1% or 1.34/0.88= +52.2%

--> theoritical new DPS = 7.6*1.2645 = 9.61 sen

Catalyst II:

Further upside potential in dividend and capital play in 2011/12. PKNS plans to further injects around RM 500M worth of properties into ARREIT in 2011 bringing ARREIT asset value to RM 1.8B. Current asset value is RM 1B, RM 1.3B after the 3 properties injection.

Abolition of 10% WHT for local ikan bilis/ big fish investors in budget 2011?

Weekly chart. There was a 4 weeks selldown in Apr/May. Followed by 3 mths sideway accumulation with increasing vol and higher high candles. Floor&Ceiling has also formed. This is what attracted my attention in the first place :)

This week closed with bullish macd divergence above ceiling. Expecting it to visit recent high of RM 0.925.

Salient details:

Listed on 26 February 2007, par value RM 1.00

Currently own 15 properties.

Current DPS around 7.6 sen, or 8.5% gross yield at RM 0.880 entry.

Catalyst:

PKNS injecting 3 properties valued at RM 270M into ARREIT with expected Q410 completion. Partial new share, partial cash payment. Not sure if the 3 new properties are yield accretive, but back of the envelope calculation (which is likely flawed) revealed so much...

New share issue: 122,727,273 @RM 0.880

Existing share issue: 573,219,858

Loan drawdown: RM 162M

*Assumption - new properties yield 8.5%

current market cap: 573,219,858*0.88= RM 504.43M;

market cap increase: (270-162)/504.43= +20.41%;

issue increase: 122,727,273/573,219,858= +21%;

new cap: 695,947,131*0.88= RM 612.43M;

DY accretive: 162/612.43 = +26.45% (assuming 8.5% DY);

--> theoritical target price: 0.88*1.2645= RM 1.11 @8.5% or RM 1.34 @7.0% DY

--> theoritical cap appreciation: 1.11/0.88= +26.1% or 1.34/0.88= +52.2%

--> theoritical new DPS = 7.6*1.2645 = 9.61 sen

Catalyst II:

Further upside potential in dividend and capital play in 2011/12. PKNS plans to further injects around RM 500M worth of properties into ARREIT in 2011 bringing ARREIT asset value to RM 1.8B. Current asset value is RM 1B, RM 1.3B after the 3 properties injection.

Abolition of 10% WHT for local ikan bilis/ big fish investors in budget 2011?

Subscribe to:

Posts (Atom)